A Vertical Analysis of Financial Statements of a company, in which the amounts of individual items of the Balance Sheet or Statement of Profit & Loss are expressed in relation to a common base, is known as a Common Size Financial Statement. In this method, the figures are converted into percentages by taking Revenue from Operations or Net Sales as the base in the Statement of Profit & Loss, and Total Assets or Total Equity and Liabilities as the base in the Balance Sheet. These percentages are then compared with corresponding percentages of other periods or other firms to draw meaningful conclusions regarding financial performance and position. A Common Size Statement is useful for both intra-firm and inter-firm comparisons of the Balance Sheet as well as the Income Statement.

Common-size Statements are accounting statements expressed in percentage of some base rather than rupees.~ Kohler

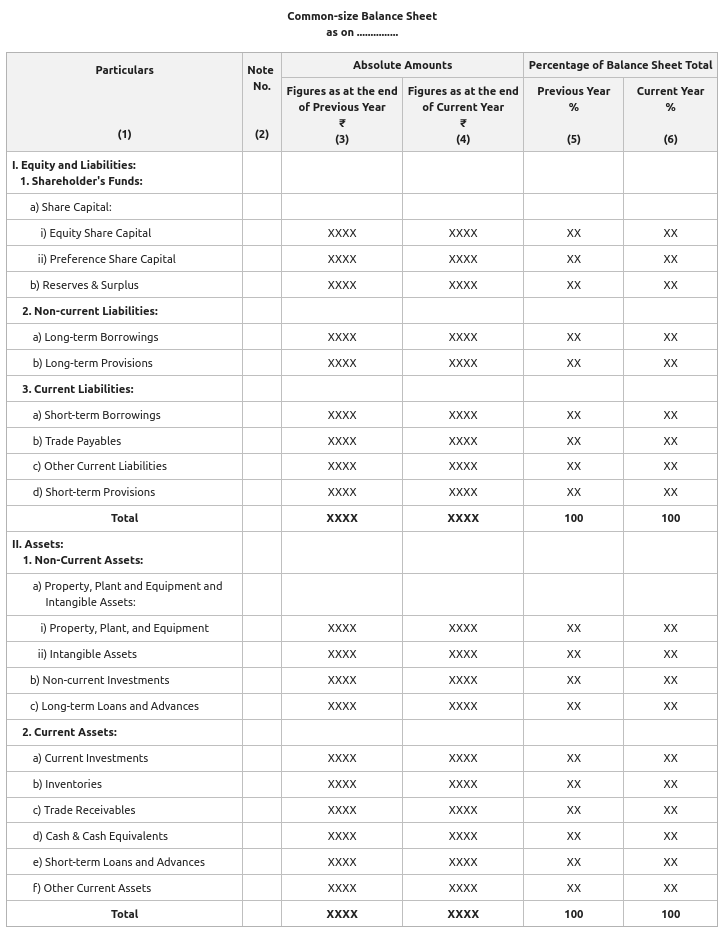

Common Size Balance Sheet

A statement that shows the percentage relationship of each asset and liability to the total assets or total of equity and liabilities is known as a Common Size Balance Sheet. In this statement, total assets or total equity and liabilities are taken as 100, and all individual items are expressed as a percentage of this total. By preparing a Comparative Common Size Balance Sheet for different periods, trends in various items can be clearly observed. When prepared for an industry, it helps in assessing the relative financial soundness of firms and provides insight into the financial strategy of an organisation.

Objectives of Common Size Balance Sheet

Different objectives of a Common-size Balance Sheet are as follows:

1. The basic objective of a Common-size Balance Sheet is to analyse the changes in the individual items of a Balance Sheet.

2. It is also prepared to see the trends of different items of assets, equity and liabilities of a Balance Sheet.

3. Lastly, it is prepared for the assessment of the financial soundness of the organisation and to understand its financial strategy.

Preparation of Common Size Balance Sheet

A Common-size Balance Sheet has the following six columns:

1. First Column: In the first column, the items of the Balance Sheet are written.

2. Second Column: In the second column, Note No. given against the line item is written.

3. Third Column: In the third column, the amounts of different items; i.e., assets, equity, and liabilities of the previous year are written.

4. Fourth Column: In the fourth column, the amounts of different items; i.e., assets, equity, and liabilities of the current year are written.

5. Fifth Column: In the fifth column, the percentage relation of the different items of the previous year's Balance Sheet to the Total of Equity and Liabilities/Total Assets are written. Here, the Total of Equity and Liabilities/Total Assets are taken as 100.

6. Sixth Column: In the last column, the percentage relation of the different items of the current year's Balance Sheet to the Total of Equity and Liabilities/Total Assets are written. Here, the Total of Equity and Liabilities/Total Assets are taken as 100.

Format of Common Size Balance Sheet

Note: The Common-size Balance Sheet does not include line items of the Balance Sheet, the accounting treatment of which are not to be evaluated.

Example of Common Size Balance Sheet

From the following Balance Sheet of Shreya Ltd. as at 31st March 2020, prepare a Common-size Balance Sheet:

Solution: