Stock prices may seem unpredictable, but they often follow patterns in data. By analyzing past prices and market indicators, we can build a machine learning model to forecast future movements. We will use CatBoost for Stock Prediction because:

- A gradient boosting algorithm that captures non-linear relationships in financial data.

- Automatically processes categorical variables without heavy preprocessing.

- Built-in techniques help improve model stability, which is critical for volatile markets.

- Faster experimentation and quicker model iteration.

- Delivers competitive accuracy compared to other boosting algorithms.

Implementation

Step 1: Importing required Libraries

Here we will import Pandas, Numpy, Matplotlib and Scikit Learn for its implementation.

import pandas as pd

import numpy as np

from catboost import CatBoostRegressor

from sklearn.model_selection import train_test_split

from sklearn.metrics import mean_squared_error

import matplotlib.pyplot as plt

Step 2: Load and Clean the Dataset

Download the dataset from here

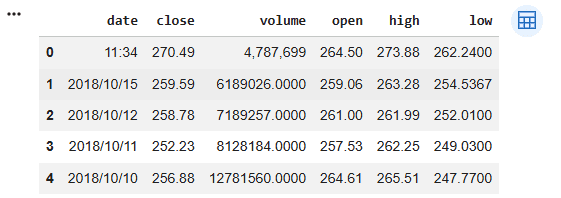

data = pd.read_csv("Your dataset path")

data.head()

Output:

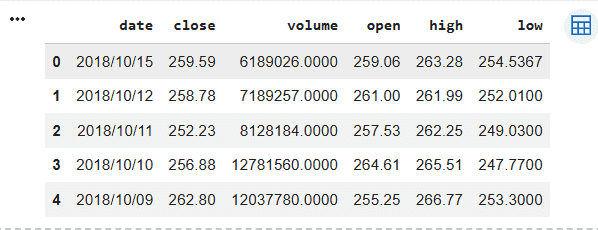

Step 3: Clean the Dataset

Remove incorrect rows and prepare the dataset for processing.

data = data.iloc[1:].reset_index(drop=True)

data.head()

Output:

Step 4: Convert Date Column and Sort Data

- Stock data must always be in time order.

- Sorting ensures the model learns from past and predicts future correctly.

data['date'] = pd.to_datetime(data['date'])

data = data.sort_values('date')

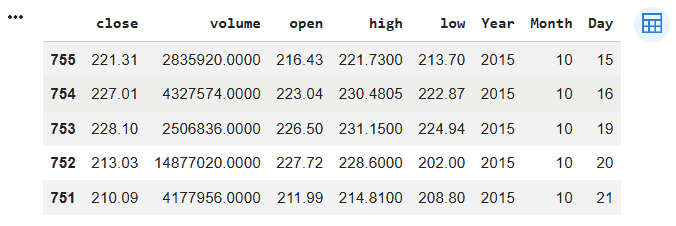

Step 5: Feature Engineering

Machine learning models cannot directly understand dates. So we extract: Year, Month and Day

data['Year'] = data['date'].dt.year

data['Month'] = data['date'].dt.month

data['Day'] = data['date'].dt.day

data.drop(columns=['date'], inplace=True)

data.head()

Output:

Step 6: Define Features and Target

Separate input variables and output variable.

- X: Open, High, Low, Volume, Year, Month, Day

- y: Close price (what we predict)

X = data.drop(columns=['Close'])

y = data['Close']

Step 7: Time Based Train Test Split

We must split the data sequentially without shuffling; preserving time order which is important to prevent future data from leaking into the training process

split = int(len(data) * 0.8)

X_train = X[:split]

X_test = X[split:]

y_train = y[:split]

y_test = y[split:]

Step 8: Train CatBoost Model

The model learns patterns from historical stock data. CatBoost automatically handles feature relationships.

model = CatBoostRegressor(

iterations=500,

learning_rate=0.05,

depth=6,

verbose=0

)

model.fit(X_train, y_train)

Step 9: Make Predictions

Predict stock prices on unseen data.

y_pred = model.predict(X_test)

Step 10: Evaluate Model Performance

Measure how accurate the predictions are:

- RMSE shows average prediction error.

- Lower RMSE means better performance.

rmse = np.sqrt(mean_squared_error(y_test, y_pred))

print("RMSE:", rmse)

Output:

RMSE: 7.203

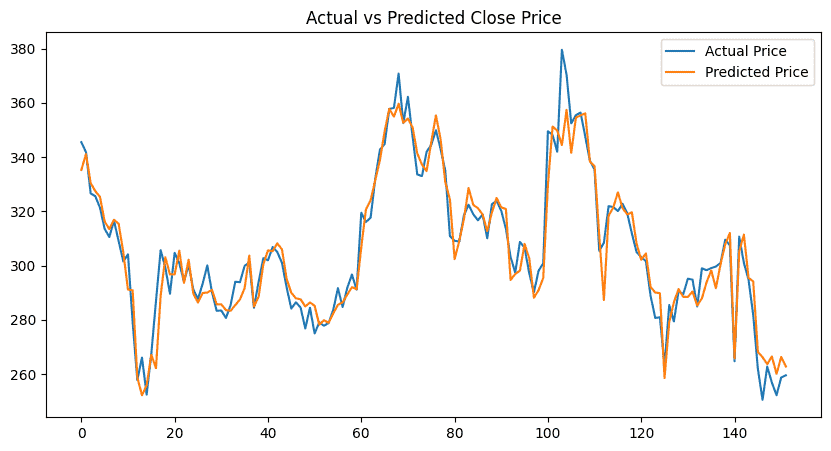

Step 11: Visualize Results

This helps visually compare:

- Real stock movement

- Model predictions

plt.figure(figsize=(10,5))

plt.plot(y_test.values, label="Actual Price")

plt.plot(y_pred, label="Predicted Price")

plt.legend()

plt.title("Actual vs Predicted Close Price")

plt.show()

Output:

Download full code from here