In statistics, kurtosis measures the tailedness of a probability distribution. It helps us understand whether the data have heavy tails, light tails or are normally distributed. Based on kurtosis, distributions can be classified into three types:

- Leptokurtic (Kurtosis > 3)

- Mesokurtic (Kurtosis ≈ 3, like the Normal Distribution)

- Platykurtic (Kurtosis < 3)

Among these, leptokurtic distributions are of particular interest in various fields like finance, risk management and quality control due to their potential to capture extreme values.

What is a Leptokurtic Distribution?

A leptokurtic distribution is characterized by:

- High kurtosis: The kurtosis value exceeds 3.

- Heavy tails: The distribution has fatter tails compared to a normal distribution.

- Sharper peak: A leptokurtic distribution exhibits a more pronounced peak near the mean.

In simpler terms, leptokurtic distributions indicate that data are prone to producing extreme outliers or rare events more frequently than a normal distribution.

Mathematical Definition of Kurtosis

Kurtosis is mathematically expressed as:

\text{Kurtosis} = \frac{\mu_4}{\sigma^4} = \frac{\left( \frac{1}{n} \sum_{i=1}^{n} (x_i - \mu)^2 \right)^2}{\frac{1}{n} \sum_{i=1}^{n} (x_i - \mu)^4}

Where:

- μ4 = Fourth central moment

- σ = Standard deviation

- μ = Mean of the distribution

A leptokurtic distribution occurs when: Kurtosis > 3

Characteristics of Leptokurtic Distributions

- Extreme Tails: Higher probability of extreme values compared to the normal distribution.

- High Peak: Sharp peak around the mean, indicating that most values cluster tightly around the central value.

- Outlier Sensitivity: Increased sensitivity to outliers, making them more common.

Example - Student's t-distribution with small degrees of freedom, it shows heavier tails.

Python Code to Calculate Kurtosis

In this Implementation, we calculate the kurtosis of a dataset to assess its distribution type

import numpy as np

import matplotlib.pyplot as plt

from scipy.stats import kurtosis, norm

data = [12, 15, 14, 17, 19, 21, 35, 45, 50, 60]

# Calculating kurtosis

kurt = kurtosis(data)

print(f"Kurtosis: {kurt:.4f}")

# Checking if the distribution is leptokurtic

if kurt > 3:

print("leptokurtic (high kurtosis).")

elif kurt == 3:

print("mesokurtic (normal kurtosis).")

else:

print("platykurtic (low kurtosis).")

# Visualization

plt.figure(figsize=(8, 6))

plt.hist(data, bins=10, density=True, alpha=0.6, color='g', edgecolor='black')

xmin, xmax = plt.xlim()

x = np.linspace(xmin, xmax, 100)

p = norm.pdf(x, np.mean(data), np.std(data))

plt.plot(x, p, 'k', linewidth=2)

plt.title(f"Histogram of Data\nKurtosis: {kurt:.4f}")

plt.xlabel('Data Values')

plt.ylabel('Density')

plt.show()

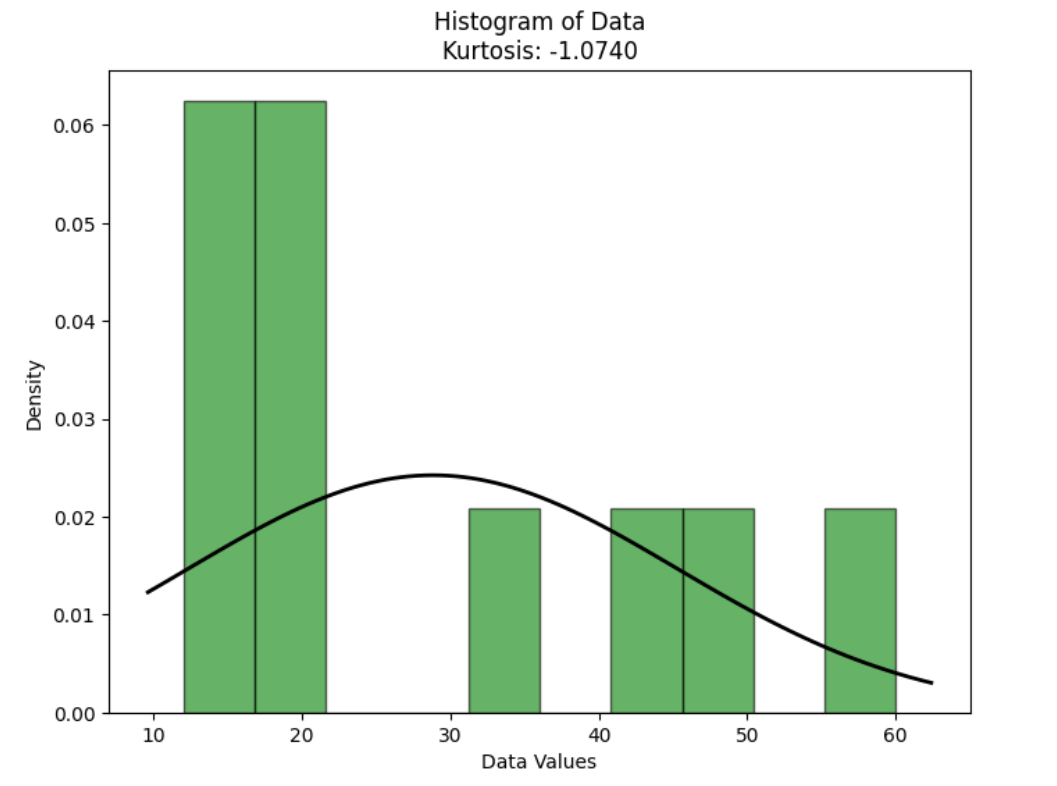

Output

Kurtosis: -1.0740

The distribution is platykurtic (low kurtosis).

Result:

- The calculated kurtosis is -1.0740, indicating a platykurtic distribution with light tails and a flatter peak than the normal distribution.

- The histogram and normal curve show a flatter distribution, confirming the platykurtic nature of the data.

Visual Representation

- A leptokurtic distribution has a sharper peak and thicker tails compared to the bell-shaped normal distribution.

- Normal Distribution (Mesokurtic): Symmetrical with moderate tails.

- Leptokurtic Distribution: High peak and fat tails, indicating high kurtosis.

Risks Associated with Leptokurtic Distributions

- Increased Uncertainty: Extreme values can distort standard statistical models.

- Misleading Inference: Traditional statistical techniques assuming normality may fail.

- Underestimation of Risk: Risk models may underestimate potential losses due to extreme events.

Leptokurtic vs. Mesokurtic vs. Platykurtic Distributions

Property | Leptokurtic | Mesokurtic | Platykurtic |

|---|---|---|---|

Kurtosis | > 3 | = 3 | < 3 |

Tails | Fat | Moderate | Thin |

Peak | Sharp | Normal | Flat |

Outliers | More Frequent | Moderate | Less Frequent |

How to Detect Leptokurtic Distributions

- Kurtosis Test: Use statistical tests like the Jarque-Bera test to detect high kurtosis.

- Graphical Methods: Histograms and QQ-plots can visually highlight heavy tails.

- Skewness-Kurtosis Analysis: Analyze skewness and kurtosis together to assess asymmetry and tailedness.

Applications of Leptokurtic Distributions

- Finance and Risk Management: Modeling asset returns to predict the likelihood of rare events.

- Quality Control and Manufacturing: Identifying processes with high variability and extreme outliers.

- Environmental Studies: Studying rare environmental events such as earthquakes and hurricanes.